Between the socialist millennials who want everything to be open access and free to the affluent travelers who can pop off to Mykonos at the drop of a hat and the spendthrift seniors paying for nursing care with Medicaid, LGBT folks run the gamut when it comes to money, their access to it, and beliefs about it. A new survey from Experian offers some interesting insight.

We think we save more than we do

Asked to characterize their habits on a zero-to-10 scale, with zero denoting "spender" and 10 denoting "saver," more than half (52 percent) of LGBTQ respondents placed themselves in the 6-to-10 "saver" range.

But responses to more detailed follow-up questions gave a decidedly different impression:

* 44 percent of LGBTQ respondents said they struggle to maintain adequate savings versus 38 percent of the general population.

* Just over one-third (34 percent) said they have bad spending habits that they'd like to improve or change versus 28 percent of the general population.

* LGBTQs estimated they devote 16 percent of monthly income to discretionary spending but just 11 percent to saving or investment.

It's worst for millennials, ages 25 to 34

* 53 percent of respondents in that age group reported struggling to maintain savings.

* 49 percent disagreed with the statement "I am in control of my finances" versus a range of 56 to 58 percent of those aged 35 to 64 and 75 percent for those 65 and up.

* 49 percent of the 25- to 34-year-olds reported having bad spending habits--a condition that diminishes with "remarkable consistency among members of older LGBTQ age segments."

Our financial priorities

* 29 percent save for retirement.

* 20 percent are paying off debt.

Money (or lack of) equals stress

A recent survey by Honeyfi, a budget app that helps couples manage their money together, asked 300 LGBTQ-identified couples about their money issues. They found that 82 percent of couples worry about money at least once a month, with 58 percent of respondents admitting to feeling anxious at least once a week.

Are you spending too much?

The survey showed that LGBTQ people "find it more important than their non-LGBTQ counterparts to set aside money for entertainment."

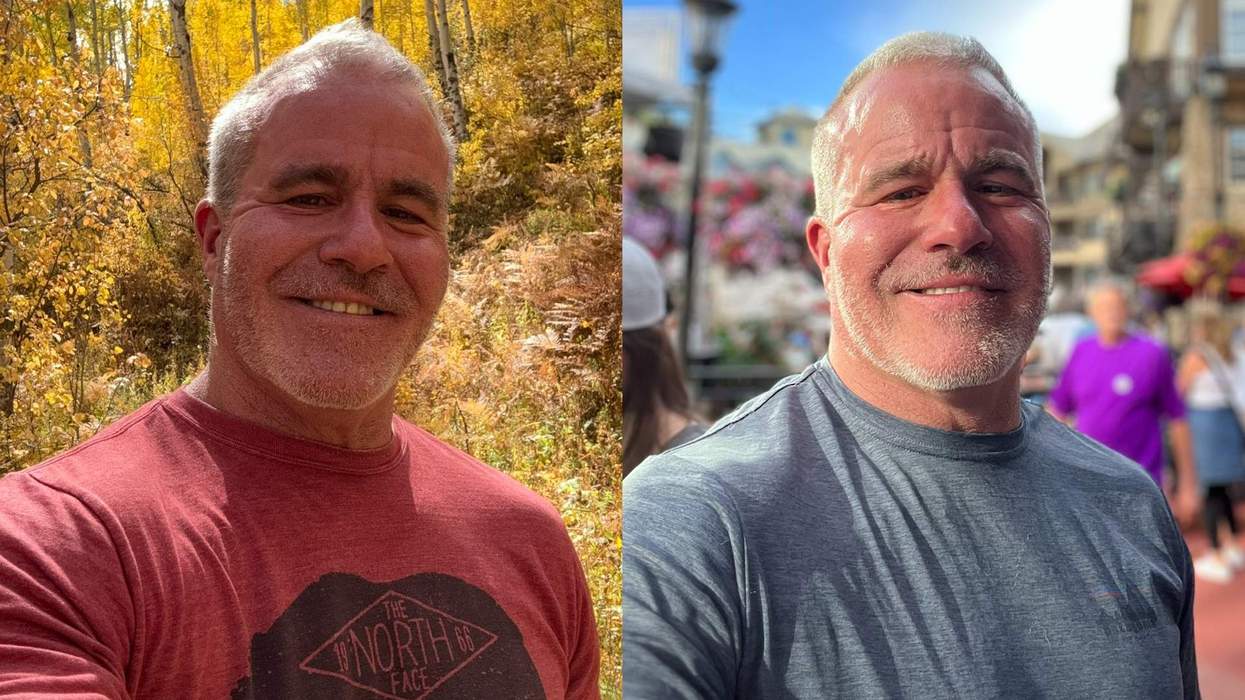

"It boils down to priorities," says David Rae (pictured below), a certified financial planner specializing in the LGBT community. "If you look online at financial planning sites, one of the first things they talk about is saving for kids' college education. Since many [in the LGBTQ community] don't have children, they've got way more money to spend on housing or a car or travel."

Those between the ages of 25 and 44 spend more on nearly every category (from clothes to entertainment, fitness, hobbies, dining out, and partying) except for one: travel. LGBTQ respondents over 65 prioritized travel more than any other other age group.

LGBTQ respondents in the 25- to 34-year-old age group reported overspending at significantly higher rates than older counterparts in the areas of personal hygiene (26 percent), clothing (38 percent), and dining out (53 percent). But 46 percent of all LGBTQ respondents said they spent too much money dining out. "Eating is often a matter of going out for a great meal with your friends, not just feeding your family," Rae says.

What plastic?

Twenty-five percent of those 25 to 34 (and 18 percent of LGBTQ respondents overall) have no credit cards at all.

How the rest of us use cards

* 70 percent use them to purchase necessities.

* 55 percent use them for rewards (like cash back, hotel stays, or airline miles).

* 32 percent of all age groups say they use credit cards to improve or build creditworthiness, with 50 percent of LGBTQ respondents age 25 to 34 giving that reason.

Bias and discrimination

A significant majority (62 percent) of LGBTQ respondents reported having experienced financial challenges because of their sexual orientation or gender identity.

Discrimination impacts our finances

Ten percent of all LGBTQs have experienced lower salaries, 12 percent were passed over for a job, 13 percent faced harassment or discrimination at work.

Source: Experian online survey (May, 2018).

Retirement Is Going to Happen

Retirement savings has never been a hot topic among LGBTs, in part because much of the community (trans women, gay and bi men) have historically died prematurely thanks to violence, cancer, and AIDS-related conditions. Many battle economic disparities, such as the lowered earning potential of two-women households faced by lesbian and bi women, or the high unemployment rates trans men experience. That doesn't leave a lot of room for reitrement planning.

The LGBT world "definitely faces some challenges in retirement," says financial blogger David Rae (DavidRaeFP.com). "Many don't have children who can help care for them as they get older. Some are also disconnected from their families and cannot count on support from siblings or other relatives."

That's why the need to save. Rae answers two common questions about saving:

Say I'm in my 20s and saddled with student loans. Should I save for retirement or pay off the loans first?

"Student loans are stressful, I get it," says Rae. "But don't ignore saving for retirement. If you put away just $2 per day and get an employer match over your entire career, you will retire a millionaire.

"At the very least, save enough to get your full employer match. From there, look at paying down your student loans. Don't freak about paying off your student loans as fast as possible. Set a time frame to have them paid off, figure out the payment to get there. Set up automatic monthly payments and then forget about it."

What if I'm 50 and haven't saved a penny for retirement. Am I doomed?

"There is always room to improve your retirement," Rae offers. "Starting at 50, you will be playing catch-up. You will need to find ways to sock away serious money. Look at how you can cut back on expenses. Consider working a bit longer. Take advantage of tax-favored accounts like a 401(k) or IRA."

Rae adds that the first step is dismissing the idea that you don't need a financial planner. A media fixture who has appeared in Time and on MSN Money, Marketplace, and NPR, Rae is the son of NFL quarterback Mike Rae (who played for the Oakland Raiders) and learned about money from his dad -- and by watching his dad's fellow players fail to plan. Now a volunteer with AIDS/LifeCycle Ride (where his team has helped raise $1 million), Rae says it's not true that only the wealthy can afford financial help.

"Everyone can benefit from working with a financial planner," he insists. "There are planners who specialize in working with people just getting started saving or paying down debt. Many people can find tips and advice on the internet to get started, but many others will never get started if they don't have someone like a financial planner holding them accountable."

Why Marriage Really Matters

Nobody wants to be roped into a loveless marriage, but hey, if you are together for the long run, tying the knot could save you a lot of money down the line. Same-sex couples now qualify for Social Security benefits after a year of marriage, which is money that's been long denied to LGBT couples. Here are the facts:

* You can get spousal benefits after you turn 62 and your partner is receiving retirement or disability benefits. If you claim these benefits (the amount is usually about half of your spouse's full retirement benefit) before you turn 67, the amount you get is lower than if you wait it out. Take benefits by 70, because there's no advantage to waiting after that. You can still claim spousal benefits even if you aren't eligible for Social Security yourself (like if you were a stay-at-home parent or you worked for a company that didn't pay into the SS system).

* If you claim spousal benefits, it doesn't impact the dollar amount your spouse gets at retirement. If you have kids (either under 18 or full time K-12 students who are older and disabled), they may also qualify for Social Security benefits.

* Even if you are now divorced, as long as you were married for a decade or more, you may still qualify for your former spouse's benefits. (It's complicated, so see an adviser and do note that usually once you remarry, your benefits situation will change.)

* If your spouse dies, and you've been married at least nine months, you can collect Social Security survivor reduced benefits starting at 60 years old, or full benefits at your full retirement age.

* If you're divorced and your former spouse dies, you might still qualify for survivor benefits (you must have been married a decade as well).

* If you have kids under the age of 16 or one who is disabled of any age, you would receive survivor benefits, and kids of the deceased who are under 18 and in school or disabled would also qualify for survivor benefits (they need to be unmarried still).

Another Reason to Marry?

Ron Stone, a Los Angeles CPA whose firm, LGBT.tax, focuses exclusively on taxes and other financial issues for the LGBT community, told Nerd Wallet that a benefit of being married is not getting hit with the gift tax. If you give someone more than $14,000 a year and you aren't married, that money will be taxed. So, if you and your bae don't have a wedding license but do have, say, a joint checking account and you put in more than $14,000 last year, the money could be considered a gift. "If the IRS audits and decides they want to look at things a certain way, they could argue it's a gift and you could be subject to a tax," Stone says.

Make It Rain

According to The LGBT Financial Experience, a report published by Prudential, based on a 2016 survey, LGBT respondents were more likely to consider themselves spenders, compared to the general population. For some queer folks, spending is a way to impress unaccepting family members ("Hey, mom, look, I'm successful. Do you love men now?"), while other spending is merely to keep up with their peer group.

"Everyone knows the stereotype of 'keeping up with the Joneses,'" says financial planner David Rae. "Well, there are gay Joneses too. [For some], having the latest iPhone or iWatch or car or whatever can begin to feel like a necessity."

Must-Try Digital Helpers

Credit Sesame

Keeping an eye on your credit score is important and it can be difficult finding the right servicer to do so. Credit Sesame is a simple and free app that you can download onto your mobile device. It can help you keep an eye on your credit score and alert you when the score goes up or down, when a creditor reports something, and more. Credit Sesame is a great tool because you can check on the most important credit factors and your borrowing potential, while also getting your score free from TransUnion with monthly updates. The app (CreditSesame.com) also helps you determine if you are paying too much on credit cards and loans. The main benefit of an app like Credit Sesame is that it gets rid of the middleman of credit reporting agencies. With those, you usually have to wait for emails or letters in the mail to let you know how you're doing. With Credit Sesame, it is a simple tapping of the screen.

Bill Shark and Trim

These do similar things: Bill Shark (BillShark.com) will negotiate with your satellite and cable providers, internet providers, home security, and subscriptions to lower your bills. It keeps 40 percent of the savings, which seems like a lot but isn't if it's something you don't have time or energy to do yourself. Trim (AskTrim.com) will also renegotiate your internet and cable bills and analyze your subscription purchases to see if you want to cancel any. It takes 33 percent of any savings.

Tune In to Learn

Queer Money

Finally, a show that focuses on the specific financial nuances of LGBT folks. Queer Money -- a podcast started by gay couple and personal finance bloggers, authors, and speakers known as the "Debt Free Guys," David Auten and John Schneider -- was actually inspired by their own money problems. Despite being financial experts in their careers, Auten and Schneider fell victim to many of the same everyday money mistakes we all make, and at one point found themselves overwhelmingly in debt. Together, as life and business partners, they managed to climb their way out of the hole (and stayed out) by developing a plan of four basic principles: 1) Use Cash, 2) Live Below Your Means, 3) Have a Financial Plan, and 4) Be Money Conscious. Their story was recently published by Yahoo! Finance in "How We Fell in Love and Climbed Out of Debt as a Gay Couple." (Podcast.DebtFreeGuys.com)

Afford Anything

Think financial planning requires meetings with stuffy old guys in banking suits? Nope. Afford Anything host Paula Pant dials down the financial lingo so the average listener can understand. Not only is Pant passionate about the subject, she helps her guests understand that financial planning goes beyond balancing a checkbook and making a budget. Pant's no-nonsense podcast should inspire confidence that you can make better decisions with your money and your time.

(Podcast.AffordAnything.com)

Spend Money to Make Money

More people are outsourcing chores with apps like Task Rabbit and Instacart, but feel guilty about it. You shouldn't. A new study of 6,000 people from Harvard Business School and the University of British Columbia says that spending money on time-saving activities (aka reducing the time you do yard work, clean your apartment, or purchase groceries) is more likely to increase your happiness than buying material purchases (like cocktails, clothing and swag, even makeup and video games). The study's lead author, Harvard Business School professor Ashley Whillans, says spending money to save on your own time "correlated the most with higher life satisfaction and decreased stress across all incomes."

Even better? "We do see that time-saving purchases actually benefit ... the lowest-income people the most," she told reporters, "potentially because they're most pressed for time and money."

Beware the Student Loans

Though financial experts says we shouldn't worry about having student loan debt, many queer folks clearly do, according to a new survey called "State of LGBTQ+ Finances: Student Debt, Retirement Savings, and More." On average, LGBTQ borrowers have $112,607 in student loan debt -- that's $16,000 more than the general population's $96,211 in loans.

A majority (60 percent) say they regret taking on student loan debt, compared with only 45 percent of the general population. That could be because LGBTQ borrowers are more likely to make less than $50,000 a year. More than half (53 percent) reported making less than $50k.

Source: Student Loan Hero, 2018

Money Can't Buy Love or Happiness

$75,000

The amount of annual income in which people are happiest. Making more than that did not raise happiness. Making less than that lowered happiness.

85%

The percentage of Americans who felt happy every day, regardless of their income.

Source: Angus Deaton and Daniel Kahneman, Princeton University's Woodrow Wilson School,who analyzed surveys of 450,000 Americans polled by Gallup and Healthways in 2008 and 2009.